OCEN (Open Credit Enablement Network) is the new buzzword in the Indian fintech industry right now and for valid reasons.

To explain this terminology in detail, let us associate it with a few examples. Let’s go back in time when Tim Berners-Lee and his team shaped the future of the Internet with HTTP. Or the days when clunky landlines paved way for slick mobile phones or recently, what UPI did to digitise the Indian payment system.

OCEN (or Open Credit Enablement Network) is just about that! A new age credit infrastructure that allows applicants to connect with lenders with zero baggage.

Let’s dive deep into it and understand what OCEN is all about, how it all started, what does the future hold for it, what will it look like, and so on.

What is OCEN (Open Credit Enablement Network)?

Let’s face it. Even today, loan application is one of the most tedious processes out there. With mounds of paperwork, the time taken, and the high chances of rejection, the loan approval process often turns the applicants away, forcing them to enter the debt trap of loan sharks. Imagine - paying 20% rate of interest every month!

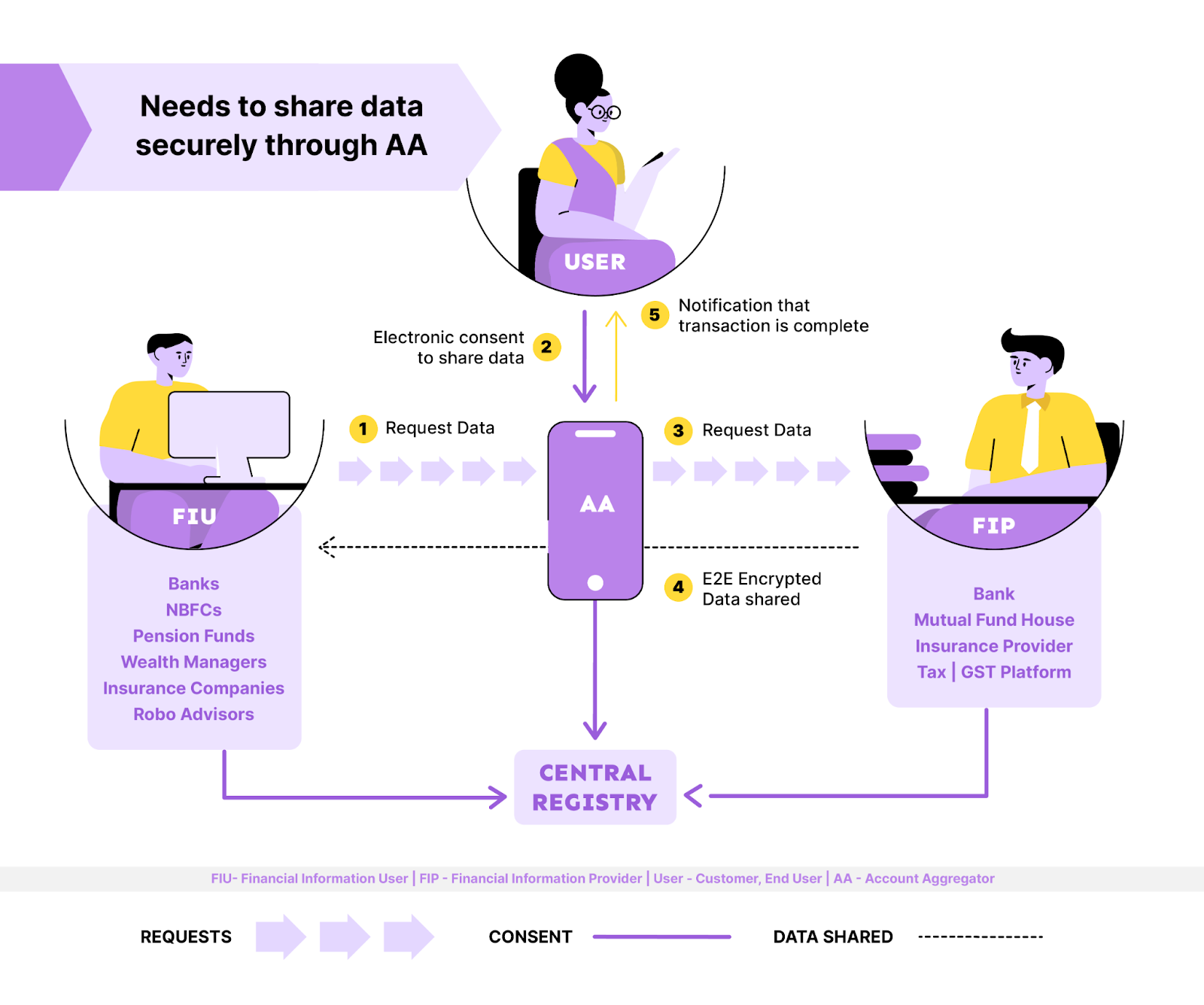

That’s where OCEN (Open Credit Enablement Network) comes into the picture. It is the Indian version of the existing Open Banking system which is quite prevalent in Europe.

It is an ecosystem which will help agencies to become loan service providers (LSP) and will let loan services be offered beyond the restricted domain of banks, NBFCs and other financial service institutions.

What that means is that in the near future Zomato, Swiggy, PhonePe, Paytm, Oyo, Airtel and every other service provider you use can become a Loan Service Provider and can offer you credit.

In fact, when the founding architect of Aadhaar and Infosys cofounder, Nandan Nilekani, announced the launch of OCEN in July 2020, he clearly said that it will be on the same credit structure as that of UPI — smooth, seamless, and secure.

How did OCEN start and come into the limelight?

Imagine driving to your destination. One path is congested with traffic and the other is a freeway, which one would you prefer?

OCEN is the freeway to the credit line you are looking for. This no hindrance pathway is integral for a country like India where inaccessibility is often the cause behind the ruptured credit line work.

For instance, an entrepreneur say Suresh, resides in a remote rural area of Tamil Nadu with limited access to banks, and runs a small scale automotive parts manufacturing unit. Let’s say, he is in need of credit but due to the lack of proximity to financial institutions, he is unable to secure the funding he needs.

He is left with one of these two options: Loan money from the loan shark and succumb to the high interests or succumb anyway due to lack of funds.

Interestingly, OCEN is his way out of this maze, thanks to its ease of access anywhere in India and democratised approach to credit.

While it can quench the prevalent credit thirst, it can also solve a much bigger problem of the credit distribution problem. With the help of OCEN, people like Suresh can secure their loan from legit banks - or 10 other apps on their smartphones, with zero paperwork, and at a nominal rate of interest, much like funding with zero paperwork.

All of this buzz started when Nandan Nilekani announced the OCEN (Open Credit Enablement Network) protocol, where he affirmed that it will include every prerequisite to become an ideal fintech disruptor—data analytics, artificial intelligence, and machine learning. And while these may sound like buzzword right now, OCEN's success will depend on how LSPs use these technologies to offer loans of all shapes and sizes in the future.

Interestingly, OCEN will be launched experimentally via a reference app called Sahay, which is available to all the MSMEs that are registered with the GeM (Government e-Marketplace) portal.

Here are some problems with the conventional credit line and what OCEN will be able to solve:

- High interest credit

- Manual intervention which is prone to error

- Lack of one-stop destination for all documentation

- Time consuming and costly credit distribution network

- Time consuming paperwork and background verification process

- Limited reach. Many SMEs do not reside in tier-1 and even tier-2 cities. Many creditworthy borrowers live in tier-3 regions as well

What does the OCEN protocol say?

OCEN defines a common and simple language which Lenders and LSPs (Lender Service Providers) can use to do two things with respect to loans and loan applications:

- Exchange data

- Interpret data

The OCEN protocol is designed by keeping 7 crucial guiding principles in mind and goes by the acronym MODEALS (Minimalism, Openness, Diversity, Embeddability, Agnosticism, Layered Innovation, Security):

Minimalism: Though the OCEN protocol enables different loan products, the objects and application process is standardised and defines only the components that serve as common denominators to all loans. Say, for instance, the lender, the borrower, the interest rate, the loan amount, and the terms.

Openness: OCEN protocol is designed in a way for open APIs to aid interoperability and inclusion. This prevents the need for bilateral and proprietary connections between capital providers and LSPs as well as being a bottleneck for accessibility. This means once a LSP implements the respective API specifications, it gets instant access to every lender that has implemented the OCEN protocols, and vice versa.

Diversity: When it comes to size, technological adoption, products and services being offered, the ecosystem of MSME is “extremely diversified.” Interestingly, OCEN is created to be super extensible, allowing the players of the ecosystem to collaborate, innovate, and meet the needs of this finance sector.

Embeddability: OCEN is designed to keep the loan application process embeddable within the platform. This allows borrowers to take the advantage of a digital lending interface with the brands or companies they already trust.

Agnosticism: This is more from a “technical” standpoint where interoperability and flexibility between the credit products and technology implementations are met. This enables the new market players to offer different services to the members.

Layered Innovation: With Indian stack, OCEN protocol focuses upon 3 foundational layers—Aadhaar card (for Identity), Account Aggregators (for Data Authorisation), and UPI (for Processing Payments).

Security: Most importantly, OCEN protocol enforces strong encryption and authentication requirements to shield the data of the entire loan lifecycle.

OCEN design considerations

Now that this topic is in trend, here’s a million dollar question—what will OCEN look like?

While there have been lots of speculations about what OCEN will look like for borrowers as well as lenders, we at Parallel, think that its framework relies on the following factors:

1. Security

Money matters and so does the digital transaction method. Users today are aware and are more likely to drop the payment process if they find any discrepancies in the authentication process. The trust factor builds up only when there is a glitch-free user experience.

The ease of usage and speed, while clear enunciation of the process in simple and legible words is what makes the security factor trust-worthy. Instructions in the vernacular languages are the cherry on top.

2. Convenience

In this world of instant gratification, no one has the patience to wait. This is why people stopped standing in queues to pay their bills and moved on to applications like Google Pay and Phone Pe to get their job done.

The OCEN network will be held to similar standards of convenience.

Will it take too long? Is the platform asking too many questions? These are the common convenience based questions that can be posed by the consumers. They are more likely to stick to their original methods if the new technology does not make things easier.

It is important to highlight the main difference between OCEN and other existing credit lending networks is that while the time taken to set up a request for credit is similar, the latter takes at least 5-7 working days to process your loan application.

However, with OCEN, the information is flowing seamlessly and therefore approvals are happening in real time, thanks to the account aggregators. Account aggregators, as we discussed in our previous blogs, are like last mile delivery service providers but for data.

3. Clarity

Nobody has the time for convoluted messages. It is interesting to note that clarity and security are intrinsically linked.

In terms of clarity, here are two important factors users always look for:

- Is this a complicated platform?

- Am I able to understand the procedures involved?

The platform is supposed to be easy to understand, even in layman terms because that is the target audience. So the framework of OCEN is meant to be clear with simple language, data process, and work-flow, akin to following guided signs along the road.

The second thing is the degree of understanding. If a user is to try a new platform, that too a financial platform involving sensitive information, he/she needs to understand what they are stepping into.

Not having a clear sense of processing might lead to them abandoning the platform for more conventional means. The way to avoid this is to break down the process in sizeable chunks, not more than 5-6 steps. Keeping the content to a minimum is what will help improve the platform’s degree of understanding.

This way, the efficacy of the platform will be more profound as well as the user’s learning curve.

4. Relevance

Unfamiliarity is not welcome, especially when it comes to sensitive matters like money and credit. So before users get comfortable with OCEN-based applications, their questions are more likely to be on the lines of:

Is it meant for me?

As mentioned, UPI is now a familiar front for many, and building upon the principles of a similar app might make it less scary for the user.

This includes,

Giving context: Not everyone knows what Open Credit Enablement Network is and therefore, do not know the steps that will entail. The best way to approach this is by adding one line explanations (not more) to each step and help users understand the significance of the process.

Add more steps: Now this is a dilemma if you haven’t set the context. The user is more likely to abandon when overwhelmed with extra steps. However, if they already trust and understand the process, they are more likely to invest their time in reading up the additional steps.

3 key points to remember when designing for OCEN

We have already discussed the basic pillars on which an OCEN platform will reside - let’s explain the design involved in the framework’s development. To start with, the OCEN (Open Credit Enablement Network) framework would require the following:

1. User understanding

We have already spoken about the importance of clarity and convenience in an OCEN framework. This is interlinked with the user journey as well. From registration to uploading sensitive information, to loan application and approval/rejection, customer experience has to be seamless right until the final process.

2. The lender

While it is important for the OCEN framework to support the users, it also needs to fulfil the other end of the equation, i.e., the financial institutions that have been RBI certified.

For example, banks can leverage the OCEN network to offer loan options to borrowers across the country. This would however, require the integration of the app and the bank’s LMS with the OCEN framework. And the framework will also need to accommodate the Account Aggregators that will act as the data medium between the borrower and the lender.

3. Risk assessment and analysis

The OCEN app is, at the end of the day, a credit provider that requires transaction of money as well as sensitive information. The framework needs to be backed by an algorithm that shields this data while enabling the transfer which can be taken into account while developing the relative app.

Once implemented, OCEN has the potential to cut down the time taken for loan request and section by a substantial amount of time which can help millions in the country gain financial independence.

If we think about it, OCEN can be the need-of-the-hour during the ongoing pandemic where more and more people are desperately looking for credits to sustain their livelihoods. This one tap approach will streamline and simplify the credit process for everyone.

The future o̶f̶ is OCEN

Quick Facts:

- The digital lending market in India is poised to gain a market value of $350 million by 2023. This will have a direct impact on the share of the digital lending market from 23% in 2018 to 48% in 2023.

- As per a report,131 million MSMEs in developing countries have unmet financial needs and have a credit gap of approximately $5 trillion!

If you are thinking of building an OCEN compliant app, then you are on the right path because the Open Credit Enablement Network may have the potential to increase per revenue by 2x to 5x, thanks to the clear credit pathway.

The vision is to leverage OCEN to cater to the MSME sector, small ticket size borrowers, etc. in different parts of the country and facilitate small business owners and Next Half Billion Users of the internet to access loans anytime.

Having said that, big players can also play the role of the borrowers and set a precedence for other sectors who might be skeptical about participating in this new domain.

OCEN will also improve that standpoint of Account Aggregators that are yet to gain recognition but might become one of the most important transnational entities.

The OCEN framework will also be a benchmark of data privacy while attempting to reach the mission of adding a billion people to the credit market and therefore, improve the country’s economic viability as well.

check out these related blogs