I speak with startup founders every week who are building the next generation of financial tools. They almost always hit the exact same wall. They have brilliant financial models and robust backend systems, but their user experience feels like a rigid compliance checklist. When you are looking for the best fintech design agencies for startups, you do not need someone to just make your app look pretty. You need a partner who understands regulatory friction, trust architecture, and how to prevent users from abandoning your onboarding flow. Here is how we think about navigating this space to make the right product decisions.

10 Best Fintech Design Agencies for Startups

The best fintech design agencies for startups focus on clarity, trust, and reducing cognitive load rather than just surface-level UI. Look for teams that simplify complex regulatory requirements into seamless user habits while aligning with your core business metrics.

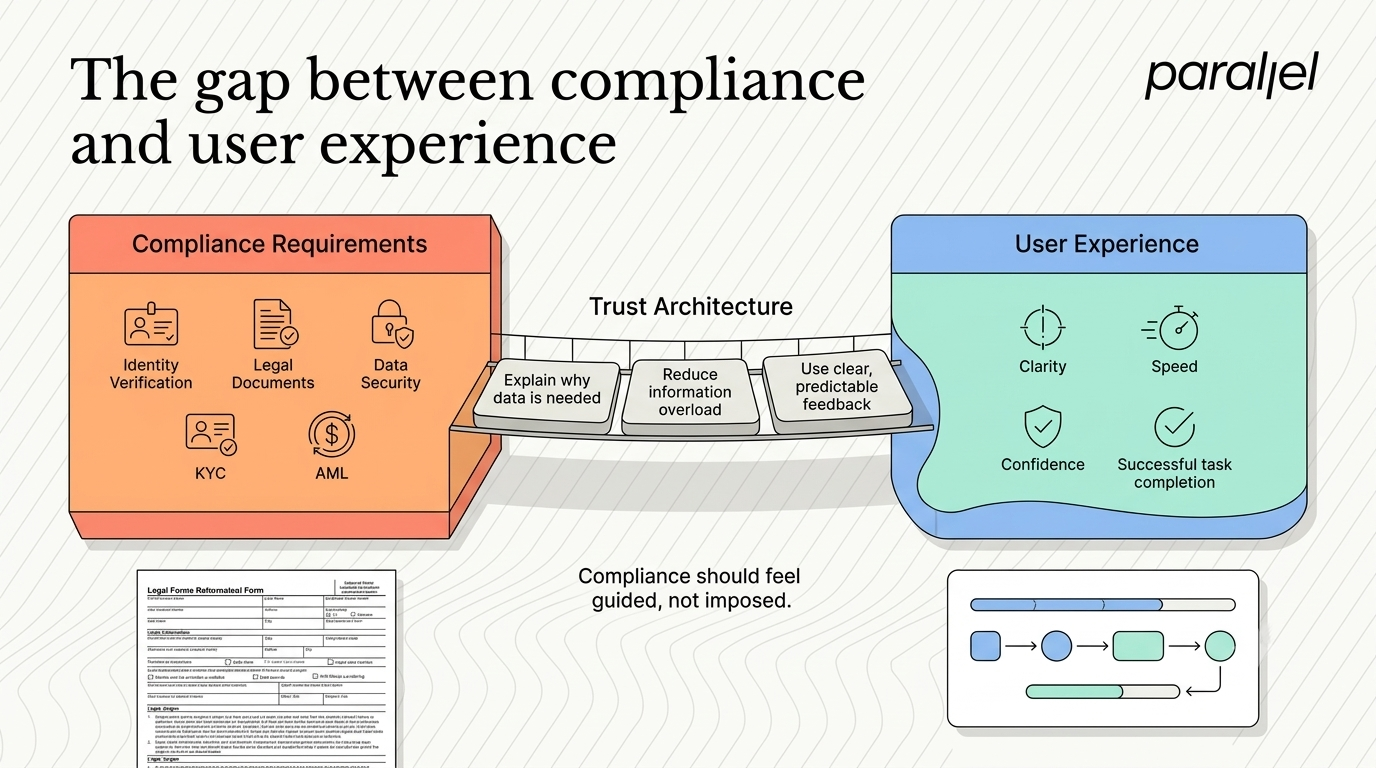

The gap between compliance and user experience

Most early-stage fintech products fail because they treat user experience as an afterthought to legal compliance. Founders often assume that if the financial mechanism works, users will tolerate a clunky interface to access it. This assumption is completely false in 2026.

Users now expect financial applications to be as fluid and intuitive as their favorite social or e-commerce platforms. However, balancing this fluidity with strict regulatory requirements is incredibly difficult. This is where most product decisions go wrong. Teams dump all their Know Your Customer (KYC) and Anti-Money Laundering (AML) questions onto the very first screen. They overwhelm the user with legal jargon. They create an environment of high friction before the user has even seen the value of the product.

According to the 2026 State of UX report by Nielsen Norman Group, basic user interface design is becoming cheaper and highly standardized. Anyone can use a component library to build a decent-looking dashboard. The true differentiator for modern digital products is structural logic and systemic trust. In finance, trust is your most important metric. If a screen looks slightly misaligned or an error message is confusing, users will not deposit their money.

We see this frequently when we conduct a UX audit for growing startups. The issues are rarely about color palettes or typography. The real problems are rooted in cognitive overload. Users are being asked to process too much information at once. To fix this, you have to design a trust architecture. You must explain to users exactly why you are asking for specific data, how it will be protected, and what they will get in return.

The onboarding crisis and the 68 percent drop-off rate

Getting a user to download your financial app is only a fraction of the battle. The real test is getting them through the initial setup phase. The data surrounding this phase is alarming. Recent 2025 research from Fenergo reveals that 70 percent of financial institutions lost clients due to slow or inefficient onboarding processes. Furthermore, Signicat's 2026 consumer data shows that 68 percent of users have actively abandoned a financial onboarding process halfway through.

These numbers highlight a massive failure in product thinking. When a user abandons a flow, they are rarely confused by the technology itself. They abandon the flow because their uncertainty has peaked. They do not know how long the process will take, they do not have the right documents on hand, or they simply do not trust the platform enough to hand over their sensitive identity data.

To solve this, we rely on progressive disclosure. You should never ask for a piece of information until it is absolutely necessary. Here is a practical approach to structuring a high-converting onboarding flow.

- Set expectations immediately: Before the user starts, tell them exactly what they need. A simple screen stating the required time and the documents needed (like a driver's license) prevents mid-funnel drop-offs.

- Prime for permissions: Never trigger native system prompts for camera or location access without context. Always use a primer screen to explain why you need the camera to scan their ID.

- Break down the KYC process: Instead of one massive form, use a step-by-step approach. Let the user complete basic details, secure small wins, and then move to document uploads.

- Design graceful error states: If an ID scan fails due to poor lighting, do not just show a red cross. Tell the user exactly what went wrong and how to fix it in plain language.

We applied these exact principles when simplifying the user experience for complex platforms. For instance, our work on Digilocker required us to rethink how millions of users interact with verified documents. By focusing on clear signaling and reducing initial cognitive load, we helped create a system that felt accessible rather than intimidating.

Retention over acquisition in modern finance

Many startups celebrate their user acquisition numbers while quietly ignoring their active usage. In fintech, day-one activation is essentially a vanity metric. If a user funds their account but never returns to make a transaction, your product has failed.

The 2026 State of Digital Analytics by Mixpanel paints a very clear picture of this dynamic. The data shows that while fintech acquisition remains strong globally, retention is what truly separates market leaders from laggards. For example, the report noted that weekly retention for wealth management apps in specific regions dropped from 91 percent to 81 percent year-over-year. This points to a market consolidation where users are ruthlessly cutting out apps that do not embed themselves into their daily financial routines.

Choosing the best fintech design agencies for startups means finding teams that design for week-four retention, not just day-one activation. You need to design for habit formation.

This starts with the First Time User Experience (FTUE). Once the user clears onboarding, what do they see? An empty state is the enemy of engagement. If they open a savings app and see a zero balance with no clear next steps, they will close the app. You must guide them toward their first meaningful action immediately.

If it is an investment app, guide them to explore a low-risk portfolio. If it is a lending platform, show them a clear, visual breakdown of their borrowing power. We focus heavily on these pivotal moments when providing fintech design services. The goal is to move the user from a state of evaluation to a state of committed usage as quickly as possible.

Moving past surface-level aesthetics

There is a dangerous trend in the design industry where agencies prioritize aesthetics over functionality. They deliver beautiful, motion-heavy screens that look fantastic in a portfolio but completely fail in the hands of a stressed user trying to transfer money quickly.

Evaluating the best fintech design agencies for startups requires looking past the portfolio. You must look at their core product thinking. Do they ask questions about your unit economics? Do they understand your regulatory constraints? Do they challenge your feature roadmap based on user research?

Big-name legacy agencies tempt many founders. While these firms do great work, they often operate at a scale and speed that does not match an early-stage startup. If you are considering a MetaLab alternative or an IDEO alternative, you should prioritize teams that embed directly with your product managers and engineers. You need agility, not just polish.

A strong design partner will push back on bad ideas. If you want to build a complex dashboard with ten different charts for a beginner investing app, a good agency will tell you no. They will help you strip the interface down to a single, clear call to action. We believe that clarity is the ultimate form of sophistication. It is much harder to make something simple than it is to make it complex.

Structuring a collaborative agency partnership

The traditional agency model is broken. The process usually involves a startup handing over a brief, the agency disappearing into a black box for two months, and then presenting a finished design that misses the mark entirely. This waterfall approach is too slow and too risky for financial products.

When startups hire the best fintech design agencies for startups, they need tight feedback loops. You cannot afford to wait weeks to see if a core interaction works. This is why we heavily utilize design sprints in our workflow.

A design sprint allows us to condense months of debate into a few focused days. We work alongside the startup founders, map out the critical user journeys, sketch solutions, and build a high-fidelity prototype. Most importantly, we test that prototype with real users before writing a single line of code.

Testing with real users exposes the flaws in your thinking immediately. You might think your new peer-to-peer payment flow is revolutionary, but a real user might find the terminology confusing. Discovering this during a prototyping phase costs very little. Discovering this after you have spent three months in engineering is a disaster.

Working collaboratively also ensures that the final designs are actually feasible. We have seen too many startups handed beautiful design files that their engineering team simply cannot build within their current constraints. By integrating product strategy consulting early in the process, we ensure that every design decision is grounded in technical reality.

The impact of AI and embedded finance

The landscape of financial software is changing rapidly. Embedded finance is moving away from being a niche concept and becoming a massive infrastructure layer. Users are increasingly managing their money directly within non-financial platforms like e-commerce sites or vertical SaaS tools.

At the same time, artificial intelligence is reshaping how users interact with their data. However, as the Nielsen Norman Group highlights, AI features can quickly become exhausting for users if they are implemented poorly. Slapping a generative AI chatbot onto a banking app does not improve the experience. It usually just frustrates the user who simply wants to check their balance or freeze a lost card.

The successful integration of AI in finance requires careful interaction design. It must be invisible, predictive, and focused on reducing manual effort. For example, an AI agent that automatically categorizes expenses and highlights unusual spending patterns adds real value. It builds trust by acting as a safeguard rather than just a gimmick.

Founders must plan for these shifts now. Your product infrastructure and your design system need to be flexible enough to adapt to open banking standards and agentic AI behaviors without confusing your core user base.

Conclusion

Building a successful financial product is incredibly challenging. You are asking people to trust you with their livelihood. Every screen, every button, and every piece of microcopy must reinforce that trust. If you overcomplicate the experience, users will leave. If you hide behind jargon, users will leave.

Finding a partner to help you build this requires looking for depth. You need a team that has seen these problems play out in real time and knows how to navigate them. You need strategic clarity, grounded research, and a relentless focus on the user's actual behavior. Let your product's simplicity do the talking.

Frequently asked questions

1) What defines the best fintech design agencies for startups in today's market?

In today's market, top-tier partners are defined by their ability to balance regulatory compliance with intuitive user experiences. They do not just create attractive interfaces. They focus heavily on trust architecture, cognitive load reduction, and deep product strategy. They understand that a beautiful screen is useless if it causes a user to abandon an onboarding flow.

2) How much does it typically cost to hire a specialized partner?

Costs vary wildly based on the scope of the project, the complexity of the app, and the agency's location. A focused sprint or an initial minimum viable product design might range from twenty to fifty thousand dollars. Comprehensive platform redesigns can exceed six figures. It is vital to evaluate the cost against the potential return on investment from improved retention and reduced user drop-off.

3) How do we compare the best fintech design agencies for startups against hiring freelancers?

Freelancers can be great for executing specific visual tasks or filling temporary gaps in your team. However, an agency brings a multi-disciplinary approach. When you hire a specialized firm, you get product managers, UX researchers, and UI designers working in tandem. This collective expertise is crucial for tackling the systemic complexities inherent in financial software.

4) What is the typical timeline for designing a new financial application?

A focused discovery framework or design sprint can yield actionable prototypes in just a few weeks. However, designing a full, production-ready application usually takes anywhere from three to six months. The timeline depends heavily on the complexity of the feature set, the speed of stakeholder feedback, and the intricacies of the required compliance flows.

5) Is it the right time for us to hire the best fintech design agencies for startups?

The right time is usually right before you write code for a major new initiative. If you are preparing to build your core application, pivot your product direction, or if your current analytics show a massive drop-off in user onboarding, you need strategic design help. Bringing a team in early prevents expensive engineering rework later.

6) How do we measure the return on investment for UX improvements?

You measure ROI by looking at strict behavioral metrics. Track the percentage increase in successful onboarding completions. Monitor the reduction in customer support tickets related to confusing interface elements. Most importantly, measure the changes in user retention during the critical first thirty days. Good design directly impacts these numbers.

7) What exactly is trust architecture in design?

Trust architecture refers to the structural decisions that make a user feel secure and confident. It involves using clear language instead of legal jargon, explaining exactly why data is being collected, providing transparent error messages, and ensuring the interface responds predictably. It is the psychological foundation of any successful financial product.

8) Why is ParallelHQ considered among the best fintech design agencies for startups?

We earned our reputation because we focus strictly on clarity and product thinking rather than superficial trends. We have partnered with early-stage teams to simplify incredibly complex systems into usable, everyday tools. By prioritizing real user behavior and actionable strategy, we help founders build products that actually survive in the market.

check out these related blogs

.webp)